![Image Trump tariffs miss the mark on why some U.S. industries are failing [Lima Charlie News][Photo: Brendan Smialowski / AFP]](https://limacharlienews.com/wp-content/uploads/2018/06/Trump-tariffs-miss-the-mark-on-why-some-U.S.-industries-are-failing.jpg)

The Trump administration’s heavy tariffs on iron and steel will have very little impact on China, while punishing the industries of longtime U.S. allies. The problems of a failing U.S. steel industry will not be solved by tariffs alone.

In March, the Trump administration announced that there would be an across-the-board introduction of increased tariffs on the importation of steel and aluminium into the U.S. The stated reasoning was the need to “rebuild” steel and aluminium production in the U.S., and to restore jobs and the domestic supply of these two broad ranges of products.

President Trump relied upon federal law, the Trade Expansion Act of 1962 (first signed by President John F. Kennedy), that enables the president to increase or reduce tariffs on goods deemed critical to national security.

President Kennedy had remarked upon signing the Act:

“This act recognizes, fully and completely, that we cannot protect our economy by stagnating behind tariff walls, but that the best protection possible is a mutual lowering of tariff barriers among friendly nations so that all may benefit from a free flow of goods. Increased economic activity resulting from increased trade will provide more job opportunities for our workers. Our industry, our agriculture, our mining will benefit from increased export opportunities as other nations agree to lower their tariffs.”

Initially, certain exemptions were granted by the Trump administration to longtime trading partners and allies Canada, the European Union and Mexico. The exemptions, however, expired at midnight on May 31st, with no reprieve from the administration. A trade war quickly escalated with immediate threats of retaliation from the E.U., Canada, and Mexico.

President Trump responded tweeting, “FAIR TRADE!”

FAIR TRADE!

— Donald J. Trump (@realDonaldTrump) May 31, 2018

Tensions escalated further at the 44th G7 summit, held in Quebec June 8-9th. At the summit leaders reaffirmed retaliatory measures against the tariffs, and Trump refused to endorse the G7 communique. Trump lashed out at Canadian PM Justin Trudeau following his departure via tweet.

Based on Justin’s false statements at his news conference, and the fact that Canada is charging massive Tariffs to our U.S. farmers, workers and companies, I have instructed our U.S. Reps not to endorse the Communique as we look at Tariffs on automobiles flooding the U.S. Market!

— Donald J. Trump (@realDonaldTrump) June 9, 2018

PM Justin Trudeau of Canada acted so meek and mild during our @G7 meetings only to give a news conference after I left saying that, “US Tariffs were kind of insulting” and he “will not be pushed around.” Very dishonest & weak. Our Tariffs are in response to his of 270% on dairy!

— Donald J. Trump (@realDonaldTrump) June 9, 2018

The results of the tariffs have been immediate. According to FOX Business, “American steel prices have skyrocketed since Trump announced tariffs of 25% on steel and 10% on aluminum in early March.”

Yet, even a cursory examination of the market indicates that these tariffs will not restore these industries to a condition of autarky or create the types of jobs the rhetoric promises.

Before addressing the impact of these tariffs on U.S. trade it would be useful to understand just why the U.S. iron and steel industries have failed to maintain themselves as viable industries in recent years.

The Cost of U.S. Iron and Steel Production Is Just Too High

A primary reason the U.S. iron and steel industry failed to prosper is that U.S. production had a fatal flaw. The principal raw material used for the production of iron and steel, high-quality hematite iron ore, was exhausted after World War II, leaving a much lower quality source. That meant processing required higher cash inputs to make these low quality iron ores compatible with modern steelmaking.

During the early iron-producing eras of the 19th and early 20th century the U.S. produced its iron from the high-quality hematite iron ores available in northern U.S. mines around the Great Lakes. These hematite ores contain about 70% iron. These deposits are commonly referred to as “direct shipping ores” (DSO) or “natural ores.” Increasing iron ore demand during World War II dramatically reduced the availability of these high-grade hematite ores in the United States. This meant that US producers had to use lower-grade iron ore sources, principally through the utilization of magnetite and taconite (with an iron content of only 25-30%). Prior to World War II, taconite was considered an uneconomic waste product.

The mining of taconite involves moving massive amounts of ore and generates massive tips of waste products. The waste comes in two forms, non-ore bedrock in the mine (the overburden or interburden locally known as ‘mullock’), and unwanted minerals which are an intrinsic part of the ore rock itself (‘gangue’). The mullock is mined and piled in waste dumps, and the gangue is separated during the beneficiation process and removed as tailings. [i] Taconite tailings are mostly the mineral quartz, which is chemically inert. This material is stored in large, regulated water settling ponds.

This taconite is of such poor quality that it has to be concentrated (‘beneficiation’). The ore must be ground into a fine powder where magnetite is separated from the gangue by strong magnets. The powdered iron concentrate is then combined with a binder such as bentonite clay and limestone as a flux. As a last step, it is rolled into pellets about one centimetre in diameter that contain approximately 65% iron. The pellets are fired at a very high temperature to harden them and make them durable. This is to ensure that the blast furnace charge remains porous enough to allow heated gas to pass through and react with the pelletized ore. [ii]

Even more importantly, the health and environmental costs of producing and using taconite ores is very high.

The Costs of Mining and Processing to Our Health and Environment are Too Great

The crushed waste rock from mining and processing taconite ores was dumped into the rivers and the lakes. These wastes showed up in Lake Superior, the source of drinking water for many cities. On April 20, 1974, a US District Court judge ruled that the drinking water and Lake Superior must be protected from the asbestos-like particles generated by this waste disposal. The Reserve Mine was forced to begin disposing of tailing wastes on the land, and to implement air pollution control equipment, instead of discharging them directly to Lake Superior. This became one of the costliest pollution prevention cases in US history.

The cost was even higher for the workers who mined and handled taconite. A 2003 study concluded that the most likely cause of 14 of the 17 cases of mesothelioma (cancer of the lung) among miners on the iron range was contact with asbestos or asbestos-like particles. Since that study was concluded, 35 additional cases of iron range miners with the disease have been diagnosed.

Mesothelioma occurs at twice the expected rate among the population of the north-eastern region of Minnesota. The lengthy epidemiological study of Minnesota iron miners concluded in December 2014 that those working 30 years in the iron mines had a lifetime chance of having a mesothelioma of 3.33 cases per thousand people, more than double the background rate of 1.44 cases per thousand people.

![Image Iron-miner’s lung - This lung section is from a 76-year-old man who spent most of his working life mining iron ore. The black pigment is hematite. [National Museum of Health and Medicine]](https://limacharlienews.com/wp-content/uploads/2018/06/iron-miners-lung.jpg)

The history of the coal, iron and steel industry has often demonstrated the indifference and complicity of the mine and mill owners in the destruction of the occupational health and safety of the workers in them. Mining coal, iron ore, and operating liquid iron and steel plants has killed and maimed many of those engaged in that industry and destroyed the towns, villages and cities in which they lived. It wasn’t just the health effects of working taconite ores which brought about the restrictions on its use. It was also the terrible health effects on the miners, their communities and the environment.

Mining coal and iron, operating blast furnaces, and transporting these substances has been a stain on the industrial landscape since its earliest days. Progress in mining could be judged by the worsening condition of the miner’s and blast furnacemen’s lungs. There were many more miners and iron and steelworkers killed by the dust than in any mining disaster that occurred with such great regularity. Black lung, pneumoconiosis and mesothelioma were regular effects of working in these industries.

In 1978, I wrote a study for the International Metalworkers’ Federation, “Health Hazards in the Iron & Steel Industries,” and was in contact with the Mineworkers’ Union. They were having trouble getting compensation for a number of miners in Harlan County, Kentucky. They had shown the X-rays of the lungs of some of the miners to the company doctors. The doctors looked at the X-rays and stamped them “Normal”. Frustrated, the union sought relief for their workers in court. The judge asked the doctors how they could stamp “Normal” on lung X-rays where all of the expert witnesses showed that these workers in fact had Black Lung and mesothelioma. One doctor said, “Well around here, that’s normal.”

When I see a ton of steel being imported I think of the lives and health of the workers who are not breathing in the dust of the ores or inhaling the fumes or suffering the high heat of the steel mills.

In China, the world’s leading producer of steel, air pollution is so extreme that in 2015, it was estimated to contribute to 1.6 million deaths per year in the country. Smog pollution is heaviest in the industrial provinces of Shanxi (coal mining) and Hebei (steel production).

The solution to America’s Rust Belt is not giving workers the right to die of occupational diseases again, or living in polluted and toxic environments. It is using the savings made on imports to re-educate the workers in new technologies and non-toxic jobs.

The problems of the mines and mills are also the problems of the environment. I bemoan the fact that many of the unions who are rejoicing over the Trump tariff initiatives, are deaf to cries for improved health and safety at their jobs. The Trump reorganisation of OSHA has left too few inspectors to protect those whom they are engaged to protect. Many southern states are attracting the polluting industries to their area, where worker protection is at its lowest.

So, there is more to the question of “restoring manufacturing jobs” than just weighing up of the economic and political consequences of the tariffs. The occupational health and environmental concerns should be an active part of the discussion.

A tariff is a tax, plain and simple. In this case, it’s an unnecessary tax on every American family and a self-inflicted wound on the nation’s economy.

– Matthew Shay, National Retail Federation President / CEO

The Tariffs Alone Will Not Have the Intended Effect

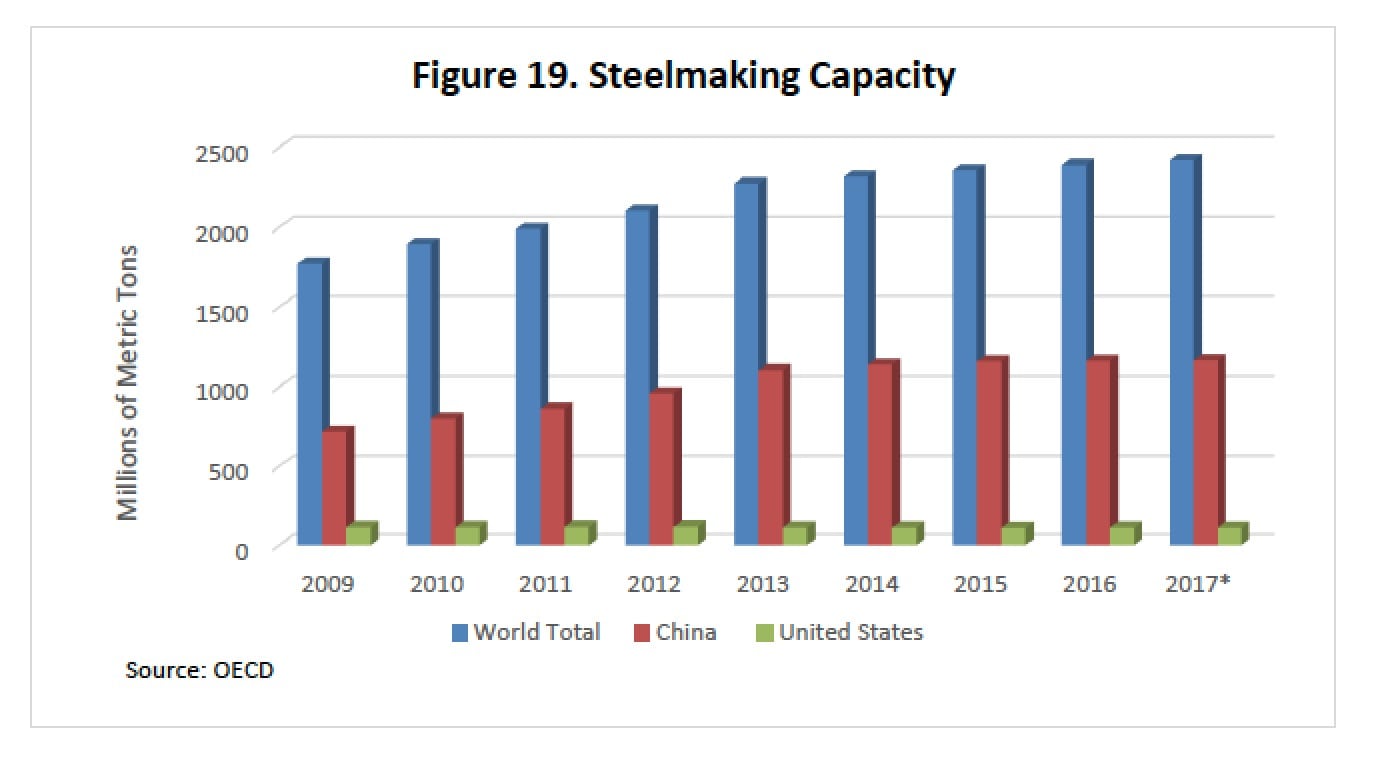

The higher costs (economic, environmental and occupational) became a heavy burden on the competitivity of the industry, so the import of readily available iron ores began to rise. U.S. iron production became even less competitive with the modernising of the steel-making process. The bulk of the newer steel capacity in the U.S. has been produced using electric arc furnace (EAF) technology, which is sourced from feedstocks predominately derived from nearby scrap steel supply.

In addition, two of the biggest hurdles in the global iron-ore mining industry are transportation costs and ore quality. U.S. iron-ore suppliers have suffered on both fronts – being far away from key seaborne Asian markets and producing essentially a high-cost pellet product.

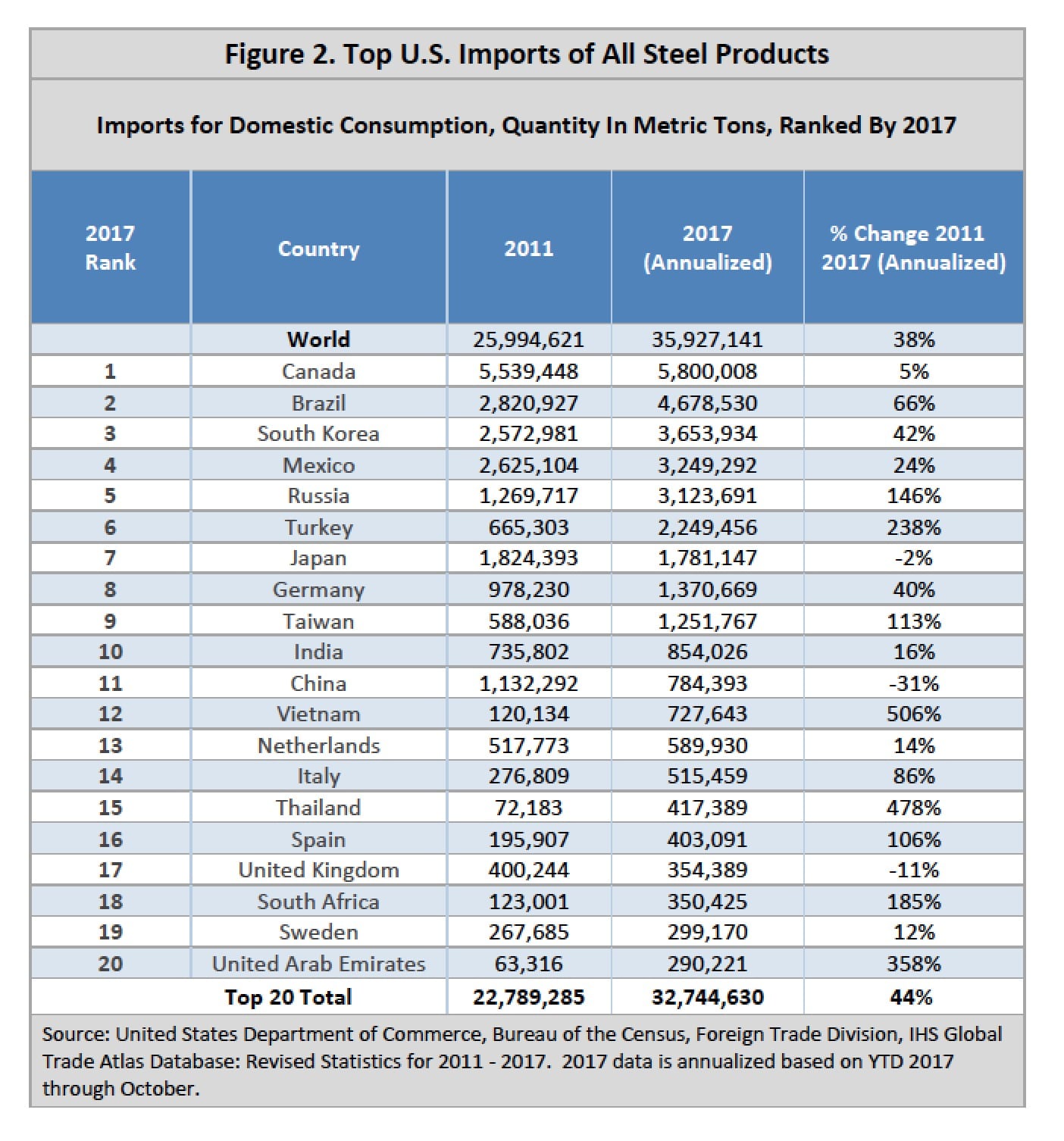

Meanwhile, U.S. iron-ore imports have had a diminishing impact on domestic supply. In 2005, the U.S. imported just over 12-million tonnes of iron-ore, mostly from Canada and Brazil, which accounted for 23% of domestic consumption. In 2015, this percentage dropped to 12%.

Historically, U.S. iron-ore production has been highly concentrated among two or three large producers. In 2015, integrated steel and mining company ArcelorMittal USA, steel producer US Steel, and iron-ore mining company Cliffs Natural Resources, accounted for 94% of domestic supply. This was mainly because of their control of iron ore production, linked to large, integrated, steel production mills. In the international steel industry, the market is dominated by three producers, BHP Billiton Ltd., Rio Tinto Group and Vale SA.

However, the largest global producer of steel is China. In August 2017, China produced 74.6 million tonnes of crude steel. Not only was that a record high, it also topped the 69 million tonnes produced by the 66 other nations monitored by the World Steel Association.

According to the Macquarie Group, China accounted for 80% of all steel growth, and 90% of all seaborne iron ore demand growth, in the years between 1980 to 2016. Australia has been China’s major supplier of iron ore. According to data from the Australian Bureau of Statistics, the value of Australian iron ore exports to China in 1996 stood at $2.91 billion. By 2006 — just one decade later — that figure swelled to $14.37 billion. Fast forward another ten years and the value soared to $53.755 billion.

The next largest supplier of steel has been the Indian market. In recent years, India’s crude steel production has expanded rapidly, reflecting firm economic growth and policies designed to boost the country’s manufacturing industry. Output has grown by a CAGR of 7.3% since 2010 to exceed 100mt for the first time in 2017. Production in December was sufficient to see India overtake Japan to become the world’s second largest steel producer, after China.

India is likely to cement its position as the world’s second largest producer over the coming year, with steel demand in the country projected to grow by 6% in 2018. Looking further ahead, reports suggest India’s steel production is likely to double by 2030, with the country widely expected to be the largest source of global output growth over the period.

However, because of existing trade restrictions and a high tariff on Chinese steel imports, the U.S. import market does not exhibit a high Chinese portion.

In January 2018, the U.S. Department of Commerce issued “An Investigation Conducted Under Section 232 of The Trade Expansion Act Of 1962, as Amended.” It covered “The Effect Of Imports of Steel on the National Security,” which set out the views of U.S. steel manufacturers.

[Download the full text of the report with appendices here]

The report stated:

“While U.S. steel production capacity has remained flat since 2001, other steel producing nations have increased their production capacity, with China alone able to produce as much steel as the rest of the world combined. This overhang of excess capacity means that U.S. steel producers, for the foreseeable future, will face increasing competition from imported steel as other countries export more steel to the United States to bolster their own economic objectives and offset loss of markets to Chinese steel exports.”

The investigation demonstrated the unfair trade practices of China and made a variety of recommendations.

The Secretary of Commerce recommended that:

“Due to the threat, as defined in Section 232, to national security from steel imports, the Secretary recommends that the President take immediate action by adjusting the level of these imports through quotas or tariffs. The quotas or tariffs imposed should be sufficient, even after any exceptions (if granted), to enable U.S. steel producers to operate at an 80 percent or better average capacity utilization rate based on available capacity in 2017.”

Alternatives offered included the imposition of a global tariff on all imported steel products, or just tariffs on a subset of countries (“Brazil, South Korea, Russia, Turkey, India, Vietnam, China, Thailand, South Africa, Egypt, Malaysia and Costa Rica, in addition to any antidumping or countervailing duty collections applicable to any steel products from those countries.”). Certain countries could seek an exemption, whereby “the President could determine that specific countries should be exempted … by granting those specific countries 100 percent of their prior imports in 2017, based on an overriding economic or security interest of the United States.”

Unfortunately, President Trump’s blanket tariffs, without exception, are simply not going to have the intended effect.

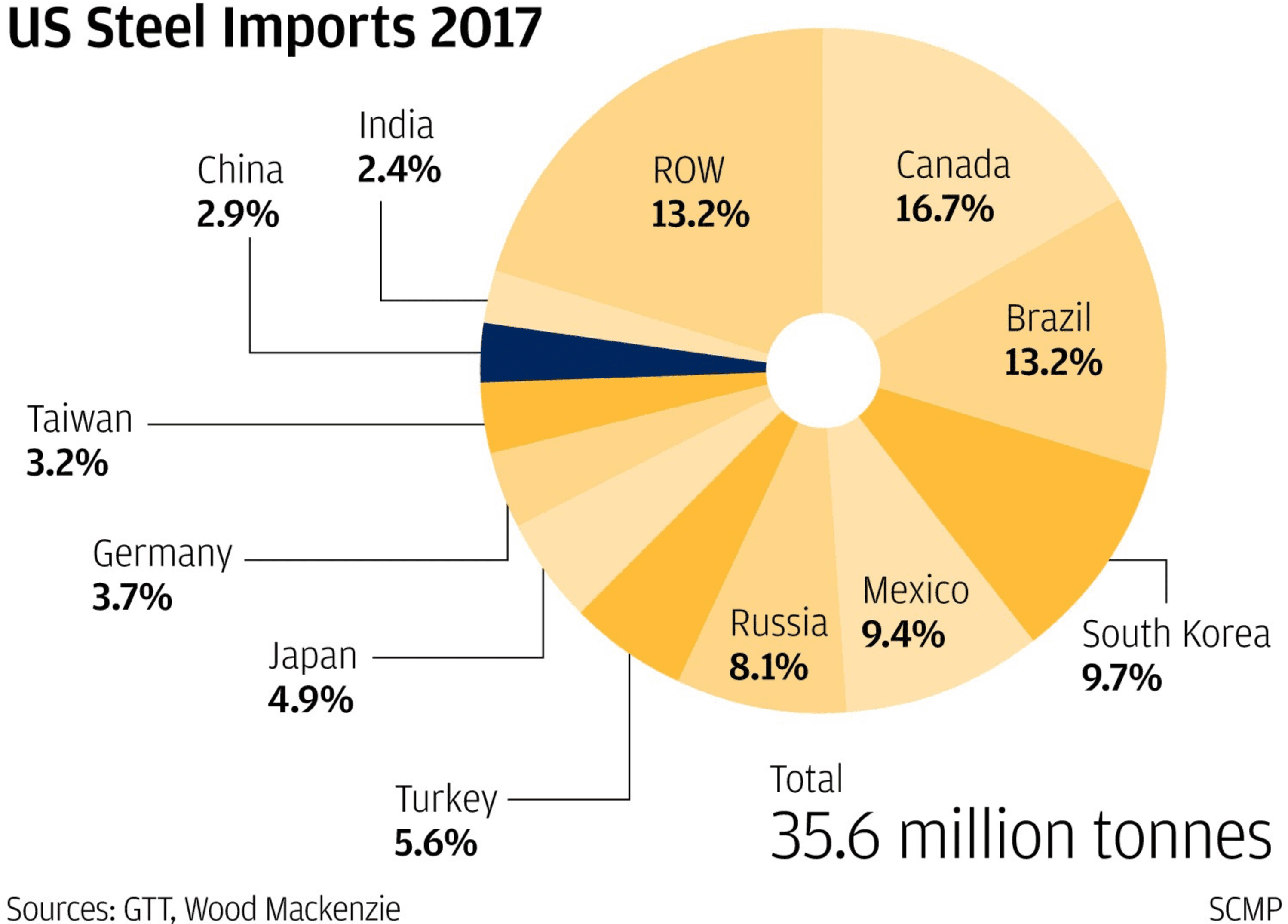

The problem is, with the U.S. only importing 2.9% of its steel from China, and 2.4% from India, placing high tariff duties of 25% on worldwide steel imports will have very little impact on China or India. Yet, such an approach will be punitive to U.S. allies. It makes no sense and will solve few problems in restoring U.S. manufacturing jobs.

What was most interesting in this study were the objections made by U.S. steel product importers to the fact that there are many steel imports which are required in the U.S. steel market (shapes, forms, tubes, etc.) which are not produced in the U.S., nor are they likely to be produced. A blanket tariff not only harms our allies, and opens the U.S. to retaliation, but it only serves to raise the price of these imports with no benefit to anyone.

According to the National Retail Federation’s President and CEO, Matthew Shay:

“A tariff is a tax, plain and simple. In this case, it’s an unnecessary tax on every American family and a self-inflicted wound on the nation’s economy. Consumers are just beginning to see more money in their paychecks following tax reform, but those gains will soon be offset by higher prices for products ranging from canned goods to cars to electronics. The retail industry is extremely concerned by the administration’s apparent desire to ignite a trade war, where the net losers will be the very people the president wants to help.” [iii]

The Northwest Seaport Alliance (NWSA), a joint venture between the ports of Tacoma and Seattle, has warned that the move could lead to broad negative economic consequences for Washington State if other nations retaliate against these tariffs. Courtney Gregoire, Port of Seattle commission president and co-chair of the NWSA, said, “We support vigorous enforcement of fair trade laws and a level playing field, but this reckless approach puts too many people and industries in the economic crosshairs.”

Don Meyer, Port of Tacoma commission president and NWSA co-chair added, “Just as concerning as these blanket tariffs is the potential for retaliatory tariffs on exports of Washington agricultural and manufactured goods. As a state in which 40 percent of our jobs are tied to international trade, we are risking jobs and quality of life by levying blanket tariffs against some of our most important trading partners and opening the door to their retaliation.” [iv] The NWSA is the second-largest export gateway for overall agricultural and forest products in the U.S. The value of those exports exceeded $6.8 billion in 2016, making up 76 percent of NWSA containerized exports.

The Trade War is Ongoing, But Controlled

Moreover, this dispute is not unique in the process of regulating international trade. This international trade war has been raging since the global financial crisis in 2008-2009.

The World Trade Organization (WTO) has been quite helpless in preventing the resurgence of protectionism or stopping developed countries from effectively impeding the WTO’s Doha Development Round (DDR). According to research by law firm Gowling WLG, the world’s top 60 economies adopted more than 7,000 protectionist trade measures between 2009 and 2016. It also found the US and EU mainly responsible for harmful trade policies! Since the GFC, the EU has adopted some 5,657 trade-restrictive measures, while the US has introduced 1,297 measures ‘harmful’ to international trade.

According to the WTO, G20 economies had implemented 1583 restrictive trade measures by October 2016 compared to around 300 eight years before, i.e., about 1300 more. Between mid-October 2015 and mid-May 2016, G20 economies applied 145 new trade-restrictive measures – averaging almost 21 monthly, up from 17 between mid-May and mid-October 2015. An earlier WTO report with wider geographic coverage found 2,557 new trade restrictions by October 2015, up 17% from the previous year.

Countries have increasingly resorted to discretionary, non-transparent, non-tariff barriers (NTBs), instead of more traditional, transparent trade barriers such as tariffs. These NTBs include subsidies, domestic content requirements, health and safety requirements, state-owned enterprises and public procurement. They involve much discretion, and greatly affect developing country exports. [v]

The main point of this is that the Trump blanket tariff imposition is an open trade barrier baldly in violation of WTO rules, so outside the customs and practices of trade disputes, that the WTO will – without doubt – find the U.S. in breach of its rules. That will open the U.S. to a raft of retaliatory measures on goods traded to the U.S. and imported from the U.S. without benefit of any protection or negotiation by the WTO.

And that is very foolish.

Dr. Gary K. Busch, for Lima Charlie News

[Anthony A. LoPresti contributed to this article]

Dr. Busch has had a varied career-as an international trades unionist, an academic, a businessman and a political intelligence consultant. He was a professor and Head of Department at the University of Hawaii and has been a visiting professor at several universities. He was the head of research in international affairs for a major U.S. trade union and Assistant General Secretary of an international union federation. His articles have appeared in the Economist Intelligence Unit, Wall Street Journal, WPROST, Pravda and several other news journals. He is the editor and publisher of the web-based news journal of international relations www.ocnus.net.

Lima Charlie provides global news, insight & analysis by military veterans and service members Worldwide.

For up-to-date news, please follow us on twitter at @LimaCharlieNews

[Main Photo: Brendan Smialowski / AFP]

ADDITIONAL SOURCES

[i] Ramanaidou, E. R. and Wells, M. A. (2014). 13.13 – Sedimentary Hosted Iron Ores. In: Holland, H. D. and Turekian, K. K. Eds., Treatise on Geochemistry (Second Edition). Oxford: Elsevier. 313-355. doi:10.1016/B978-0-08-095975-7.01115-3

[ii] “Taconite”, Minnesota Department of Natural Resources

[iii] “Trump’s Steel and Aluminum Tariffs Could Harm Ports, Consumers” MarEx 2018-03-08

[iv] Ibid.

[v] Anis Chowdhury and Jomo Kwame Sundaram, “Trump’s Trade War in Perspective”, IPS 12/3/18

In case you missed it:

![Image Tariffs – a mixed blessing for American businesses [Lima Charlie News]](https://limacharlienews.com/wp-content/uploads/2018/12/Tariffs-–-a-mixed-blessing-for-American-businesses-Lima-Charlie-News-480x384.png)

![Image European Union - U.S. trade dispute escalates as E.U. issues retaliatory tariffs on a number of iconic American goods [Lima Charlie News]](https://limacharlienews.com/wp-content/uploads/2018/06/European-Union-U.S.-trade-dispute-escalates-as-E.U.-issues-retaliatory-tariffs-on-a-number-of-iconic-American-goods-480x384.png)

![Image Memorial Day may soon be a remembrance of democracy and those who had the courage to defend it [Lima Charlie News]](https://limacharlienews.com/wp-content/uploads/2018/05/Memorial-Day-may-soon-be-a-remembrance-of-democracy-and-those-who-had-the-courage-to-defend-it-Lima-Charlie-News-480x384.png)

![The Mind of Bolton - AUMF and the New Iran War [Lima Charlie News]](https://limacharlienews.com/wp-content/uploads/2019/05/Inside-the-mind-of-Bolton-Lima-Charlie-News-main-01-480x384.png)

![Image Tariffs – a mixed blessing for American businesses [Lima Charlie News]](https://limacharlienews.com/wp-content/uploads/2018/12/Tariffs-–-a-mixed-blessing-for-American-businesses-Lima-Charlie-News-150x100.png)